5 STRATEGIES FOR THE SANDWICH GENERATION

In fact, it’s likely you’re part of the Sandwich Generation.

Are you feeling pulled in multiple directions, especially between your children and aging parents? If so, you’re not alone. In fact, it’s likely you’re part of the Sandwich Generation.

According to a Pew Research Center report, adults who are part of the Sandwich Generation are those who have a living parent age 65 or older and are either raising a child under age 18 or supporting a grown child. Many provide both care and financial support to their parents and children, and 38% of those surveyed say both their grown children and their parents rely on them for emotional support.

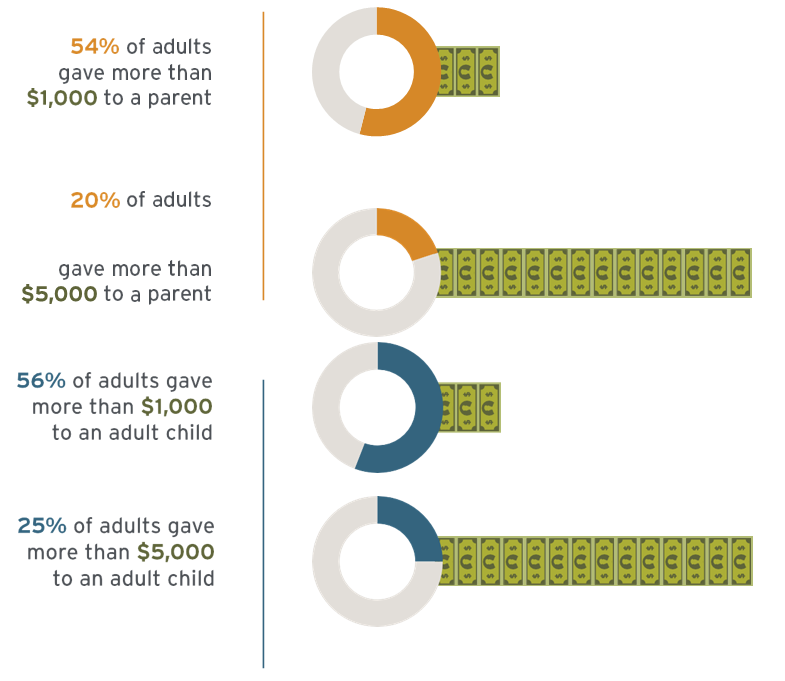

Percentage of Adults Helping Aging Parents and Adult Children

Thirty-two percent of midlife adults ages 40–64 provided regular financial support to their parents in the past year, and 42 percent expect to do so in the future. Also, half of midlife adults are still providing money to their adult children age 25 or older (51%) for basic expenses, according to an AARP survey.

FINANCIAL SUPPORT PROVIDED BY MIDLIFE ADULTS TO AN AGING PARENT OR ADULT CHILD IN THE PAST 12 MONTHS

With All This Outpouring, Who’s Caring for You?

It’s likely these added emotional and financial pressures are creating stress and hampering your retirement savings, and the only person caring for you is you.

To help enhance your well-being and grow retirement savings, following these five strategies:

1. ESTABLISH A FINANCIAL PLAN

With so much happening in your life, it’s vital to have a spending and savings plan coupled with a long-term retirement plan.

To make the most of your retirement savings (likely the reason you’re working so hard), it’s important to review today what your financial life may look like when you’re retired, i.e., retirement savings versus expenses.

Typically, financial planning is more complex for the Sandwich Generation, given your added financial obligations. Therefore, consider hiring a financial advisor who can guide you through the financial planning process, often minimizing frustration and saving you money.

Understand Where Your Money Is Going

Are you clear on how much you’re spending on your household, adult kids and parents each month? The only way to really know is to track all money coming in and going out. Start by reviewing your credit card statements, cash transfers and recurring bills, e.g., mobile phones, subscription services, insurances, etc.

FINANCIAL PLANNING TIP

When finances are intertwined with multiple family members, make financial planning a group effort with all parties following an individualized monthly budget. Also, your parents should have a retirement income plan, helping to stretch their money as long as possible, and your adult children should follow a plan that gradually removes you as a financial resource over a set timeline.

2. KEEP AN EYE OUT FOR MEDICAL AND FINANCIAL SCAMS

Older adults lose an estimated $3 billion each year to financial scams, according to the National Council on Aging (NCOA). Therefore, having frequent conversations with your parents regarding scams is important in helping to protect them financially as well as yourself, since you’ll likely be the first person they turn to if they run into financial trouble.

Some of the most common scams include callers impersonating others, e.g., an individual requesting money or asking for personal information from the Internal Revenue Service or Medicare.

The Grandparent Scam is also common, whereby a caller pretends to be a grandchild in trouble and needing money, urging grandparents to maintain secrecy.

3. COMMUNICATE OPENLY ABOUT MONEY, HEALTH AND ESTATE PLANS

For some, it’s difficult talking with parents about their money. Yet, it’s important to have open dialogue about your parents’ money, health and estate plans — before they have a health emergency and become unable to express their wishes. If you find this conversation difficult, hire a financial advisor or an estate planning attorney to lead the discussion.

Depending on your situation, you could meet independently with the advisor/attorney, or have your parents present, since sometimes it’s better for your parents to hear the news from a professional rather than their adult child.

Be sure to discuss the possibility of buying long-term care insurance — the sooner the better for more affordable rates. If this isn’t financially feasible, then the next conversation is deciding who will care physically for your parents when they no longer can care for themselves. All parties involved should be present for this dialogue, including any siblings participating in future caregiving. Agree now about your parents’ care, safeguarding family relationships later.

Finally, if you’re responsible for your parent’s estate upon their passing, know the whereabouts of all their assets, accounts (including social media) and related passwords, and ensure they’ve assigned beneficiaries.

MONEY SAVING TIP

Depending on how much caregiving you provide a parent, you may be able to list them as a dependent on your tax return. Speak with a financial professional to help determine your eligibility.

4. MAINTAIN MENTAL AND PHYSICAL HEALTH

Increased financial obligations created by aging parents and adult children can take a toll on your mental and physical well-being, decreasing your ability to help the very people you love.

Therefore, before paying another bill for a family member, first do a few things for yourself each day, including exercising, eating well, maintaining good mental health, sleeping more and saving money.

Key Benefits:

- Exercise and eating well lower the risk of disease.

- Nurturing mental health regulates feelings and increases your ability to manage adversity.

- More sleep improves your mood.

- Saving money increases feelings of happiness.

When you prioritize these activities, you improve the quality of your life and, by extension, the lives of your parents and children.

Therefore, give yourself permission to put yourself first.

SEEK A NEUTRAL THIRD PARTY

Seeking the help of a mental health professional could be exactly what you need if you’re feeling overwhelmed about simultaneously raising a family and helping aging parents.

5. MEET WITH A FINANCIAL ADVISOR

Providing financial support for your parents and children often creates financial complexity when saving for retirement. Financial advisors help optimize and streamline your financial situation based upon your specific goals and needs.

An advisor can help you:

- Understand how long your savings will last.

- Rearrange assets and accounts to minimize taxes.

- Determine pension distribution choices.

- Decide if an annuity makes sense for guaranteed income.

- Run Social Security analyses for optimal benefits.

- Coordinate a retirement income plan.

At the end of the day, a financial advisor helps you feel more confident about the financial decisions you’re making today, as you balance rising financial responsibilities that have the potential to impact your retirement. Contact us to learn more and set up a new-client consultation.

HT|TC Wealth Partners is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC, member FINRA and SIPC. Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC. All information referenced herein is from sources believed to be reliable. HT|TC Wealth Partners and Hightower Advisors, LLC have not independently verified the accuracy or completeness of the information contained in this document. HT|TC Wealth Partners and Hightower Advisors, LLC or any of its affiliates make no representations or warranties, express or implied, as to the accuracy or completeness of the information or for statements or errors or omissions, or results obtained from the use of this information. HT|TC Wealth Partners and Hightower Advisors, LLC or any of its affiliates assume no liability for any action made or taken in reliance on or relating in any way to the information. This document and the materials contained herein were created for informational purposes only; the opinions expressed are solely those of the author(s), and do not represent those of Hightower Advisors, LLC or any of its affiliates. HT|TC Wealth Partners and Hightower Advisors, LLC or any of its affiliates do not provide tax or legal advice. This material was not intended or written to be used or presented to any entity as tax or legal advice. Clients are urged to consult their tax and/or legal advisor for related questions.

Legal & Privacy | Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Securities offered through Hightower Securities, LLC, Member FINRA/SIPC, Hightower Advisors, LLC is a SEC registered investment adviser. brokercheck.finra.org

© 2024 Hightower Advisors. All Rights Reserved.